“What really matters is what you do with what you have.”

H G Wells (1866 – 1946)

90% of the world’s data has been generated and gathered in the last two years. The world is recognising us more as individuals and shaping life experiences to suit specific interests and activities. Big Data has the ability to change the way we see people, which impacts on insurance and risk pricing.

90% in 2 years?

Shoot forward from the 1980’s where the home PC was a fairly new concept and an 8-bit (1 byte) processor was a big thing. Today’s home PC stores terabytes as standard – over 1 trillion bytes. Additional to this, the internet is now available in many of our pockets.

Combine all the people today who are actively connected to the internet via computers, phones or other gadgets and using it for specific needs or interests such as:

- Communicating with others

- Searching for answers

- Researching for study or interest

- Shopping

- Streaming preferred entertainment websites, channels and programs

- Managing time and tasks

- Monitoring personal health and habits

- Planning holidays and other journeys

All this online activity is transmitted and as a result, very user-specific data is being produced and collected around the world in almost unimaginable volumes; around 2.5 quintillion bytes a day; enough to fill 10million blu-ray discs which stacked, would reach 4 x the height of the Eiffel Tower1.

It’s clear to see how 90% of the world’s data has been collected in such a short space of time2. Technology is much smarter and more accessible, and humans are more active with it as a result.

Defining Big Data

The definition of Big Data seems quite straight forward as far as the subject goes.

“Extremely large data sets that may be analysed computationally to reveal patterns, trends, and associations, especially relating to human behaviour and interactions.3.”

What’s not so clear though is how Big Data personalises people’s life experiences based on the trends of their particular interests and activity. Big Data infiltrates our lives more and more and challenges traditional privacy, as the world around us becomes more tailored to meet our apparent needs…needs that are rationally, by computational means, based on our past personal behaviour and circumstances.

Refining Life Experience

The retail industry was an early adopter of Big Data. The idea that retailers could personalise an offer for an existing individual customer based on their habits, preferences, shape or size then deliver the offer directly to the customer’s smartphone just when they happened to be a few metres away from the store used to be a pipedream. Now, it’s a simple thing of reality and consumers are well aware of it in their lives. Some find it invasive, others convenient and appealing. In any case, the true reality and the backbone of all this is the rapid emergence and value of Big Data.

Off the high street, many people search online for something only to find the very same product or service suddenly being promoted across other unrelated websites. This is targeted advertising, where Ad agencies use Big Data’s sophisticated algorithms to target an audience based on recent interests, ages or locations. Again, it’s Big Data that makes this possible and it’s very effective. Gone are the days where adverts in your favourite magazine held all the answers. There seem to be no breaks in the chain anymore…

Why is Big Data important to us?

Insurance. Being by its very nature a risk-averse industry, the insurance industry has been behind the Big Data curve to some extent, but this is changing with the emergence of Financial Technology (Fintech) and the use of digital technology in financial services. As well as Big Data, Fintech covers Robo-Advice, Blockchain technology which underpins the Bitcoin and IoT (the Internet of Things) which refers to devices other than computers which send and receive data across the internet.

The insurance industry has been pushing IoT for some time, using products like the motor sector’s ‘box insurance’ which tracks and records driver behaviour, connected home devices and wearable technology such as the FitBit – all offering ‘discounts for data’. What technology offers as a convenience, allows the providers to understand activity and behavioural patterns down to the minutest details, in turn profiling their audience more accurately and intricately than ever before.

How Big Will it Grow?

There’s broad speculation between key organisations in the industry around how many billions of devices will be connected by 2020, but if 1 byte was considered to be practical processing power in the 1980s and 90% of world data was collected in the last 2 years, there’s little doubt the volume of data processed daily is likely to increase significantly beyond the 2.5 quintillion a day we’re seeing now. The question is how? Surely there’s still more that can be connected. One could say the world is growing well, but with growth comes challenge, especially for the Insurance Industry.

What will they do with our Data?

What the insurance industry will do with all the Big Data it plans to harness is very much dependent on business strategy and consumer trends – and ultimately the skill and integrity of key individuals making key decisions within each organisation.

The intention is to improve market targeting, underwriting and pricing by enhancing customer and risk profiling – and crucially to reduce fraud which in 2014 cost the UK insurance industry £1.32 billion 20144.

Arguably, the real value of Big Data for insurers is likely to lie in:

- predicting the size and timing of future claims payouts by analysing the litigation period and payout timeframe for different types of claim and

- improving the use of resources by putting the most experienced claims handlers on what are likely the most complicated cases at the outset.

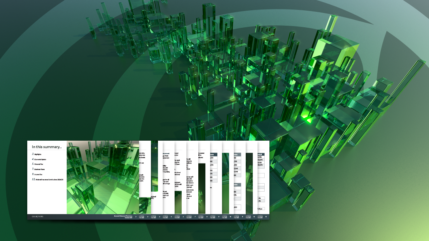

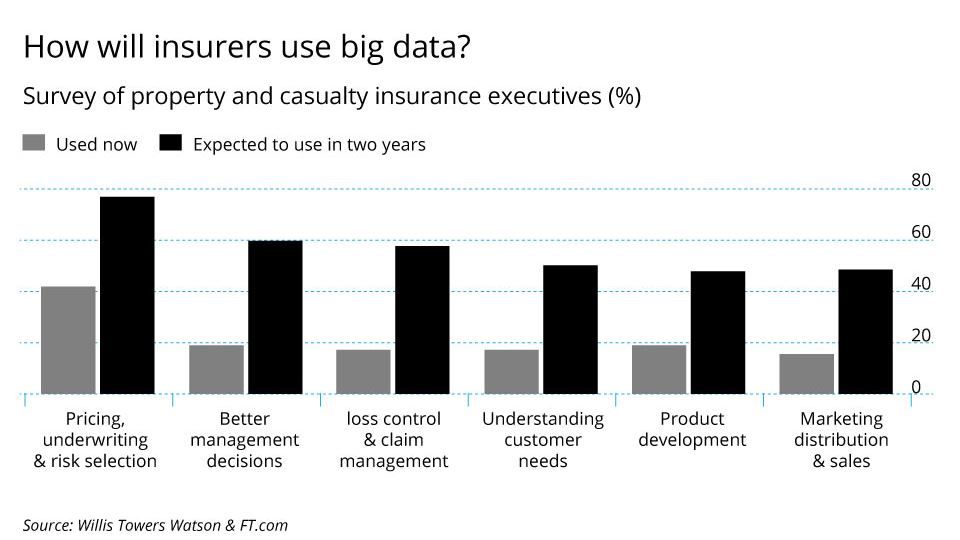

The table below shows how UK insurers intend to develop their use of Big Data over the next two years.

To this end the industry will, at the very least, monitor weather patterns, chart medical advancement and changes in patient outcomes, put sensors in our homes, and develop segmented client models by gathering data on our habits, activities and our whereabouts.

However, therein lies the root of increasing regulatory concern as insurers develop the potential to dig deeper into our lives and personal data. The issue is not so much about how much data is gathered, but rather quality of the data being captured and what is done with it. How does the ‘box’ insurer know who is driving the car?

Growing with the Flow

In November 2015 the Financial Conduct Authority (FCA) called for “views, supported by examples and evidence where possible, of how Big Data is affecting (and is likely to affect) consumer outcomes and competition in the retail general insurance (GI) sector.” The response deadline was January 2016, leading to Big Data being included as one of the FCA’s business planning priorities for 2016 /17. The FCA said it will analyse the feedback to understand how Big Data affects customers, whether it fosters competition and how the regulatory framework affects Big Data developments before deciding whether or not to “conduct a market study or take a different approach”.

This follows on from the publication ‘Disruptive influences 2.0: the Fintech revolution’, a collaboration between the CII (Chartered Insurance Institute) and Cicero Group published in July 2016 which highlights both opportunities and threats associated with Big Data. The report raises concerns that Big Data may personalise risk to the extent that it creates an uninsurable underclass by undermining the concept of ‘pooled risk’, which is a cornerstone of the insurance industry. This has already happened in areas of flood risk and could permeate through to other sectors.

As employee benefit consultants, COURTIERS’ main focus is on the Group Risk market:

- group life assurance

- group critical illness insurance

- group income protection, including employee assistance programmes to reduce absence and increase productivity in the workplace through better staff health and welfare

- group private medical insurance

So what are the implications of Big Data here? Undoubtedly the more an insurer knows about an individual or a certain group of individuals, the more precisely that insurer can price the risk. The implications are therefore complex across the group risk market as a whole. A larger database and better data analysis could be hugely influential in the development of group risk products and workplace wellness strategies, enabling insurers to better monitor changing trends in the working population and providing employers with an improved information bank to better assess strengths and weaknesses in their group risk strategy. Time will tell.