Higher levels of taxation are rarely palatable, but to adapt a famous quote ‘some forms of taxation are more palatable than others’. So, while raising tax rates is politically difficult, stealth taxes – stealthy by name and stealthy by nature, are less obvious to the naked eye and more likely to sneak under the radar.

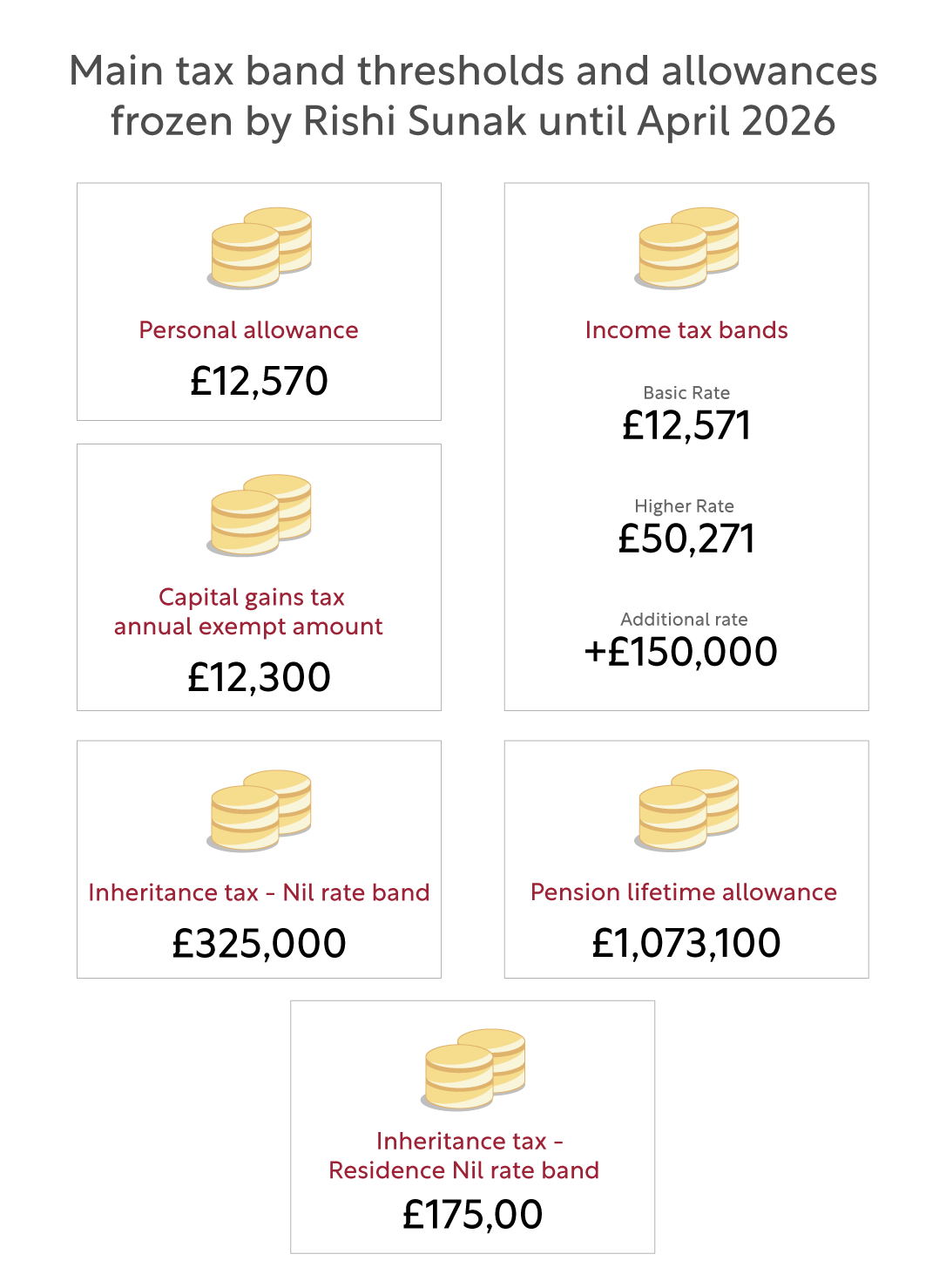

Stealth taxes are not new. But they were given a fresh lease of life by then Chancellor of the Exchequer and now Prime Minister, Rishi Sunak. Responding to the need to repair the country’s parlous finances, in 2021 he decided to freeze a whole series of tax allowances and tax band thresholds for four years from April 2022 until April 2026.

Now as the Sunak government struggles to fill the £50bn fiscal black hole left by Liz Truss’s ill-fated administration and restore fiscal stability, it’s reported that the freeze could be extended for a further two years.

More will no doubt be revealed in the Autumn Statement due to take place on November 17, an event we’ll be covering.

Stealth taxes’ best friend

The essential ingredient for stealth taxes to work is inflation. From the point of view of a cash-strapped government the higher the better, as rising nominal prices across the economy feed into higher earnings, capital gains, pensions and other assets.With allowances and tax thresholds frozen – what economists call ‘fiscal drag’ means that over the next few years millions of people will be pulled into paying tax for the first time or pushed over their existing tax threshold into a higher tax band. The longer allowances and tax band thresholds remain frozen and the higher inflation, the greater the gravitational pull of fiscal drag on people’s wealth, and the more the Treasury’s coffers swell.

With annual inflation currently standing at 10.1%, the Chancellor of the Exchequer Jeremy Hunt couldn’t have wished for better conditions for fiscal drag to do its work – or perhaps more accurately for it to do his work for him. From the Chancellor’s perspective, inflation has the added bonus of reducing the real value of the government’s debt.

Paying the cost

In October, the Institute for Fiscal Studies (IFS) calculated that by 2025-26, some 7.7 million workers could be paying the 40% rate of tax compared to 4.6 million if tax thresholds hadn’t been frozen, costing most higher-rate taxpayers around £3,000 a year. The Centre for Economics and Business Research (CEBR) reckons that taken together all the measures first introduced by Rishi Sunak will bring in an extra £46bn in revenue for the government .

If, as many expect, the freeze is extended for a further two years, the consequences would of course be magnified. The CEBR estimates this would drag another three million workers into the higher rate 40% tax band and more than double the number of higher earners paying the top 45% rate of income tax to 850,000 in 2026-27. Depending on the rate at which earnings, pension savings and asset prices rise, extending the current freeze would raise many billions more by 2027-28 .

Freezing the lifetime allowance

The effects of freezing tax allowances can be seen by taking the example of the lifetime allowance (LTA), the amount that a person can build up tax-free in pension savings before being liable to a 55% tax charge, if they take the money as a lump sum. Between the 2018/19 and 2020/21 tax years, the LTA was raised in line with inflation as measured by the Consumer Prices Index (CPI) in September of the previous tax year, but since then it has remained frozen at £1,073,100.

Had the LTA been raised in line with CPI inflation and assuming inflation of 8% and 2% in tax years 2023/24 and 2024/25 respectively, a person who had pension savings of exactly £1,073,1000 i.e. right on the LTA at the end of the 2020/21 tax year, could have added an additional £275,479 to their pension savings without triggering a possible charge.

With the freeze in place until 2026, however, were they to save this additional amount, they could face a charge of £151,513. Were the LTA be frozen for a further two years, this could result in a tax charge of more than £181,000.

Avoiding the tax net

Faced with prospect of getting dragged deeper into the government’s tax net, what actions might people wish to consider?

The list below is not exhaustive, but it might serve as a catalyst for a more detailed conversation with your financial adviser. They’ll be able to discuss all aspects of tax and tax planning with you as part of a comprehensive plan to help you and your family meet your financial and life goals.

- Work and earn less so that you don’t move into a higher tax bracket – especially if this avoids your earnings rising to between £100,000 and £125,000 when you will face an effective tax rate of 60%.

- Instead of putting more into your pension and triggering the 55% lifetime allowance charge, consider using that money to bolster your ISA (individual savings account). An ISA is a tax-efficient way of saving with all income and capital gains tax-free up to an annual limit of £20,000.

- You may be able to protect your lifetime allowance from its reduction in April 2016. Check with your financial adviser.

- If a pay rise takes you into a higher tax rate bracket, take advantage of the rules that allow you to claim tax relief at your highest marginal rate. If you’re a 40% higher rate taxpayer, this means that it costs you £600 net for every £1,000 that goes into your pension. This lowers your ‘adjusted net income’ – that’s the income HMRC uses to calculate your tax bill.

- Withdraw money from your general investment account rather than as income from your pension to take advantage of the comparatively generous capital gains tax (CGT) exemption of £12,300 a year .

- Make full use of the rules on gifting, which could allow you to reduce the value of your estate for inheritance tax purposes.

- Think about whether setting up a trust might be appropriate. A trust can be an effective way of reducing inheritance tax liability.

- You can shield your income and other wealth from tax by planning your financial affairs as a couple. One way is to make use of your spouse or civil partner’s allowances, such as the £12,300 a year CGT exemption on capital gains made outside an ISA, which effectively doubles it to £24,600.

- Spend more of your money – this can reduce any inheritance tax bill.

And finally

Given the state of the country’s finances and the reluctance of politicians to raise tax rates, stealth taxes are here to stay for the foreseeable future and look certain to feature in the forthcoming Autumn Statement on 17 November. Look out for our coverage of this important event.