“A penny saved is worth two pennies earned . . . after taxes.”

(Randy Thurman)

I recently attended a Tax Seminar and the speaker gave us ideas as to how we could work together to help our clients to mitigate tax. Let’s face it, going through the current various tax rules is not much fun and not easy to understand either, so I thought how about if I try to present it as a Game?

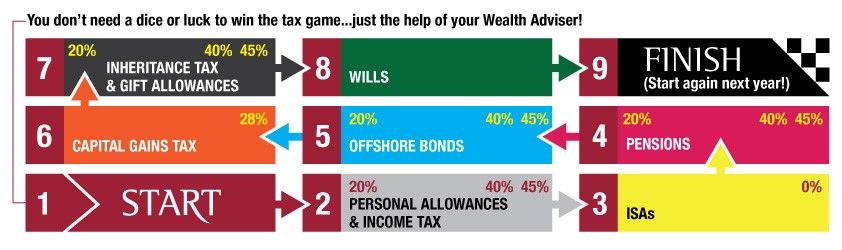

Let’s play, the rules are very simple: Look at the table below and move your investments along the board until you reach the finish line, if you follow the rules and advice before 5th April 2016, you should win.

As we approach the end of the financial year it’s always a good idea to ensure that most of tax breaks are utilised. Please be aware that the rule of “if you don’t use it you lose it” applies to most of them.

Personal Allowances: The personal allowance for 2015/16 is £10,600. In addition the starting rate of tax on the first £5,000 of savings income is zero. This is not available if taxable non-savings income exceeds the starting rate band so it is a boost to those with a total income of less than £15,600. The basic rate of tax (20%) applies to income up to £31,785 (after deducting any personal allowance).

Individual Savings Account (ISA): Take advantage of the increased limits to generate tax-free income and investment growth, but be aware that ISA’s will form part of your estate when assessed for Inheritance Tax. The maximum annual amount that can be invested in an ISA increased on 6 April 2015 to £15,240. You can invest in cash and stocks & shares, or a combination of the two, the choice is yours.

Capital Gains Tax (CGT): You can make gains of £11,100 in 2015/16 before you have to pay any CGT. Review your investments (within your risk profile) to see what proportion is held in assets that come under the CGT regime – e.g. shares, unit trusts, and investment trusts. This can be complicated, but your Adviser can help.

Any capital gains you make are added on to your taxable income to determine the rate of CGT due. Where the total exceeds your basic rate band of £31,785 (for 2015/16) the CGT is payable at 28%.

If the total is within your basic rate band, CGT is charged at 18%. You can expand your basic rate band, and limit the CGT due to 18%, by paying pension contributions or making gift aid donations before the end of the tax year.

Offshore bonds: The starting rate tax on savings income mentioned earlier also means that a greater number of offshore bond savers will pay no tax on their bond gains because chargeable event gains from offshore bonds count as savings income.

Review your pension: Radical changes last April heralded possibly the biggest shake-up to UK savings and pensions providing more freedom, choice and flexibility than ever before over how pension savings can be accessed.

Income tax relief on your pension contributions is restricted to contributions you and your employer make within your annual allowance (AA). The AA is set at £40,000, but can be extended by utilising unused allowances from the previous three tax years. However, if you have accessed your pension flexibly the AA reduces to £10,000 and you are not able to carry forward any unused allowance. You will receive full tax relief at your highest marginal rate of tax on pension contributions within your AA. Any pension contributions made by you or your employer that exceed your AA will be subject to a tax charge.

Going forward (from April 2016), pension savings (both AA and personal tax relief) will be measured across the tax year. This makes it much easier for the vast majority of clients to understand how much they can pay into their pension each year. But the interim changes could give some clients two bites at the cherry this tax year. Not everyone will benefit, but some clients will have an extra AA of up to £40,000 to use before 6 April 2016. Some high income clients will face a cut in the amount of tax-efficient pension saving they can enjoy from 6 April 2016. This might be the trigger to maximise pension funding this tax year for clients likely to be affected now or in the future. Just bear in mind the pending lifetime allowance cut to £1M from April 2016.

IHT: The new IHT Residence Nil Rate Band (RNRB), which is in addition to an individual’s own nil rate band of £325,000, is to be introduced from April 2017. This additional nil rate band is only available where the main residence is passed down to direct descendants (i.e. children, grandchildren etc). But in the meantime make sure you are making use of the annual gift allowances of £3,000 per individual (you can go back one year, if you haven’t used it). Regular gifts from surplus income could also be considered under the normal expenditure out of income (not capital) rules. Lastly, your Will is going to determine where your wealth will go, so make sure it is always up to date. With the new IHT rules kicking in soon, some existing Wills may not qualify you for the additional allowance.

The tax and pension legislative landscape rarely remains still for long and tax treatment depends on individual circumstances and is subject to change so please make sure you work with your Courtiers Adviser to take advantage of what’s available to you both now and in the future.