There’s been a huge spike over the last couple of years in people transferring money away from final salary pension schemes (also known as Defined Benefit, or “DB” schemes). Why?

The take-away

If you’re thinking about transferring your DB pension:

- Think very carefully and do your homework. There will be lifelong consequences.

- Seek advice. In most cases you’ll be legally required to.

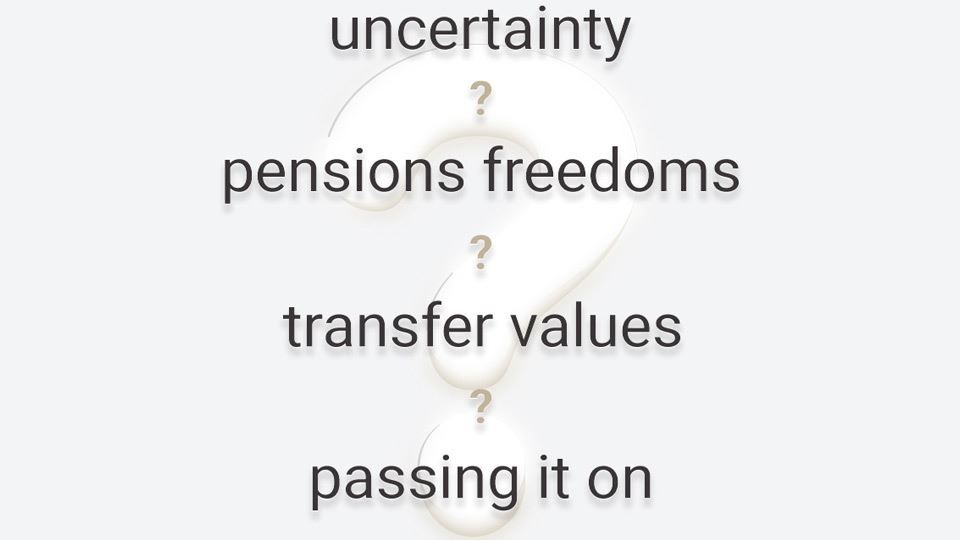

The cause of the spike

Uncertainty

Pensions have been in the news a lot recently and for all the wrong reasons.

In 2016, BHS entered administration with a £571 million pension shortfall affecting 11,000 employees.

In January 2018, Carillion went bust with its pension deficit looking likely to settle out at somewhere between £1billion and £2.6 billion – huge numbers impacting around 28,000 scheme members.

In last month’s news, the Work & Pensions Select Committee accused Tata Steel, the government and regulators of “neglecting” 124,000 British Steel Pension Scheme (BSPS) members after the employer was allowed to offload its £15 billion retirement fund amidst financial trouble.

The above alone affects the long-term financial security of more than 160,000 people.

How many more people are getting nervous about all the apparent pension doom and gloom in the news?

Where do we turn to if even the government and regulators are singled out for their incompetence in protecting scheme members?

So many questions – so much uncertainty.

Pensions Freedoms

Since the government introduced pension freedoms in April 2015, anybody aged over 55 has been allowed to access their pensions in almost any way imaginable.

This flexibility has encouraged many to access lump sums without necessarily thinking long term. Some might be acting in haste while others are picking up a hefty tax bill in the process.

Transfer Values

Transfer values offered by final salary schemes have recently reached all-time highs, leading many members to grab the money and run before anyone has a change of heart. A range of factors affect transfer values, which is another reason to make sure you’re well educated, well informed and feeling certain before making any decisions.

Passing it on

Greater flexibility over how people can pass on unused money, on death, in non-final salary scheme pensions is also encouraging people to move away.

While the list is not exhaustive it should offer a starting point for deliberations with your financial adviser.

How do you make the decision?

Here are a few things to think about, which covers only a tiny fraction of the stages we go through when helping our clients decide whether or not to transfer a DB pension.

While we can generally explain a few things, we can’t offer you specific advice without speaking to you about your particular circumstances. If you would like help with your own review, please get in touch.

What’s in a name?

This feels like a good juncture to clear up a quick point on terminology. Whilst we have more names for pensions in the UK than the Inuit people have words for snow (true story!) they ultimately break down into just two categories: defined benefit and defined contribution. This is the first thing they teach you at pension school.

With a defined benefit scheme, you know at outset what pension you will receive at retirement provided you follow an agreed path. For example, if you join your employer’s ‘60th’ scheme and work for that company for 40 years, finishing on a salary of £60,000, you know your starting pension will be £40,000 per year (40/60ths * £60,000). They are called defined benefit schemes because, at outset, the scheme has defined the benefit you’ll get at retirement. It is then down to your employer and the trustees to ensure there is enough money in the pot to pay out all of the promised pensions as they fall due. Final salary schemes fall into the defined benefit (DB) category. You could argue that the State Pension is also a DB scheme but I prefer to call it by its more proper title – the State Ponzi Scheme.

With a defined contribution scheme, on the other hand, you only know at outset what money is going to be paid in – you’ve defined the contribution, rather than the benefit. No one knows what pension might be payable at retirement because there are too many variables. Even if your employer agrees to a fixed contribution structure for 40 years, variabilities in investment returns and interest rates alone will make accurate predictions all but impossible. Personal pensions, SIPPs and SSASs all fall into the defined contribution (DC) category.

Ultimately it is the certainty of income offered by DB pensions that earned them the ‘gold plated’ status. However, as we’ve seen with the likes of BHS and Carillion, the gold plating can be very thin.

Parity of income

No one can tell you categorically whether you will be better off remaining in a DB scheme or transferring to a DC scheme. There is no mathematically perfect way to directly compare a promised future income stream with a lump sum that you might eventually convert into some sort of income stream at some point in the future. I sometimes tell people that it is like comparing apples and oranges but, on reflection, it is probably more akin to comparing apples and Liechtenstein. Professional advisers must, therefore, apply their knowledge, experience and skill to your particular circumstances to come up with a recommendation based on the balance of probabilities. Sometimes it will be a relatively clear-cut case, other times it’ll be much more nuanced.

The starting point for most people is a seemingly simple question – which route will give me more money throughout my lifetime? Tell me exactly how long you intend to live and I’ll tell you the answer! Since pensions are generally payable for life, it follows that the true answer can’t be known until you die, by which time it is all academic. In fact, the answer might not even be clear by the time you die as both DB and DC pensions have the ability to continue paying money to your next of kin for years, decades or even centuries after you’re gone. A case in point – the US Government is still paying a pension to the next of kin of a US Civil War veteran who was born in 1847! No wonder many DB schemes are desperate to encourage transfers out, even if they can’t say so explicitly. What company wants such an open-ended liability on its books?

Whilst it is impossible to know for certain, it is still possible for advisers to make reasonable assumptions about how income streams might look over a typical lifetime and, armed with this data, provide clients with a critical yield figure. The critical yield is the investment return your transferring lump sum would need to achieve, each year, within your DC pension in order to provide an income stream that’s broadly equal to the DB income you’ll give up. Put simply, what annual return will you need on your transferring money to be better off in retirement? Whilst it is useful to distil things down to a single number, there are many other factors to consider alongside the critical yield.

Flexibility of income

Another important question to ask yourself is how do you want to receive your pension?

Whilst DB pensions provide a dependable stream of largely inflation-proof income, they are usually very inflexible. They will typically pay out for the duration of your lifetime and then continue to pay an income to your spouse/civil partner on your death. If you are not married when you die, it’s often tough luck.

This model was well suited to the traditional method of retirement whereby employees walked out of the factory door at 60 or 65, carriage clock tucked under one arm and a final pay cheque under the other. Like carriage clocks themselves, this idea of a ‘cliff-edge’ retirement is falling rapidly out of fashion. More and more people are choosing to phase in retirement over a number of years, in conjunction with a gradual reduction in working hours. A DB pension can normally be deferred (delayed) beyond the scheme’s normal retirement age but, once it starts, it starts. A DC pension, on the other hand, gives you the option to gradually ramp up your withdrawals as your earned income dwindles.

Tax-free lump sums

A very attractive feature of pensions is the ability to withdraw a proportion of the fund tax-free. This payment, known as the Pension Commencement Lump Sum (PCLS), is one of the most fiercely-guarded elements of UK pensions. Both DB and DC pensions allow you to take PCLS but the way it is handled is quite different.

Within a DB pension, PCLS is usually taken as a single lump at the point your income starts. This may be helpful if you plan to use it to settle your mortgage, buy a new car or fund a world cruise but it is less useful when you have no immediate spending plans. Tucking it away into a low-interest bank account is unlikely to get anyone’s pulse racing.

Within a DC pension, PCLS is calculated in a different way and will, in many cases, be higher than the sum on offer under the original DB pension. It can also be taken in stages, as required. Some people find it useful to take a little bit of PCLS each year over a number of years to top up their ‘income’ and minimise their income tax bill, especially where they might still have earned income in the early years of retirement.

Death benefits

Whilst looking after your own needs should always be your first priority, you’ll also want to consider how your pension might support those you leave behind.

Having a guaranteed widow’s pension from a DB pension can be very reassuring if you are married at the point you retire. You should bear in mind, however, that if your spouse/civil partner dies before you then the widow’s pension is of zero value. Equally, if you are single when you retire, or even in a relationship where your partner does not meet the scheme’s eligibility requirements, your own pension won’t be uplifted to compensate for the lack of further death benefits. This is another way in which DB benefits have not necessarily moved with the times.

Because you have much greater control over your plan, the position within DC pensions is quite different. If you choose to swap your DC pot for an annuity (an income stream, paid by an insurance company, which is guaranteed for life) you can choose whether or not to include a dependant’s pension at outset. If you’re single, choosing an annuity without any death benefits means that your own starting pension will be higher.

Alternatively, if you use your DC pot for regular income withdrawals, any unspent cash can be passed to your next of kin, to be accessed in whatever format they wish. If you die before 75, such payments are usually tax free. If you die after 75 they are taxed according to the recipient’s own rate of income tax. This rule makes passing funds to non-tax-paying grandchildren very tax-efficient.

The downside:

The above are just some of the ways in which you could be better off as a result of a DB to DC transfer and you may conclude from all my comments above that I am generally in favour of such transfers. Far from it! Each case is unique and needs to be considered on its own merits. In the interests of balance, here are just a few of the potential drawbacks.

Investment risk

Whilst it is true that DC pensions offer a great deal more freedom and flexibility than DB schemes, there is one very significant price to pay for jumping ship – investment risk.

If you take a transfer lump sum from a DB pension to a DC plan you become solely responsible for any investment gains and losses from that point forward. You may choose to devolve investment decision-making to a fund manager but ultimately the buck still stops with you. If your investments perform well then you’ll do well. If they perform poorly then you’ll fare worse. On the flip side, leaving your money in a DB pension means that all investment risk is borne by your former employer. It made the promise to provide you with a pension so it remains responsible for ensuring there is sufficient money to meet its obligations as they fall due.

Capital depletion

Equally, assuming you choose to draw money directly from your DC pension at retirement (rather than swapping it for an annuity) you need to ensure your withdrawals are sustainable in the long run. In the past there were limits on the amount you could withdraw to ensure your pot didn’t expire before you did. In the post-Pension Freedom era, there are no laws protecting you from total fund depletion. This is why, at Courtiers, we insist on meeting our clients at least once a year so that we can ensure withdrawals are realistic and sustainable.

Funding considerations

The problem, as we’ve seen from the likes of Carillion and BHS, is that a very large proportion of final salary schemes are in deficit – they don’t have enough money set aside to cover the promised pensions. Most employers try to take a responsible approach to scheme funding and will agree a recovery plan with the Pensions Regulator if a deficit exists, but sometimes the trustees and employer have to take a more pragmatic approach. For example, the trustees might feel that demanding very high levels of contributions from a struggling employer would tip the employer into insolvency, which would ultimately be far worse for the members than a deficit. Many schemes, therefore, agree to long-term repayment plans on the understanding that the company will honour its side of the bargain for decades to come.

There are various methods employed by actuaries to assess how much money a DB scheme needs. Most schemes set contribution rates on the basis that the scheme will continue to receive support and contributions from the employer for the lifetime of the scheme. In this scenario, allowance can be made for future contributions and future investment growth. It is on this basis that the Carillion scheme’s deficit currently stands at ‘just’ £1 billion. An alternative measure is the full buy-out cost. This is the sum the scheme would need to hand over to an insurance company in order for the insurance company to replicate all the promised pensions. A full buy-out allows the employer to walk away from the scheme and pass all the funding risk to the insurer. Whilst most employers would love to offload DB schemes in this way, it is usually prohibitively expensive – insurers will charge a phenomenal premium to let the employer off the hook. I don’t blame them.

Companies can also be caught out by external factors which can tip an otherwise healthy scheme into deficit overnight. Countless companies have worked hard to clear deficits, only to be told by the scheme actuaries that the amount of money they need has increased since the last review because life expectancies have increased and so pensions will need to be paid for longer. It is a common complaint that employers feel they are forever chasing a disappearing horizon.

The good news is that the factors that tip schemes into deficit can reverse quickly and schemes can find themselves unexpectedly back in the black through no particular action on their part. It may not sound like good news but a finance director recently admitted to me that he did a little air punch when he heard on the news that life expectancy in the UK had started to decline again after decades of steady growth. He was thinking of his pension deficit, rather than the fact that he now had less time to live, on paper at least.

The Pension Protection Fund

It is also worth highlighting that, whilst Carillion and BHS pension members have a right to feel aggrieved, their predicament would be a whole lot worse were it not for the Pension Protection Fund (PPF).

The PPF, established by the Pensions Act 2004, has the lofty purpose of rescuing members from defaulting pension schemes. It is often referred to as the Pension Lifeboat and is funded by levies on all DB pensions. Like any insurance, riskier schemes have to pay a higher premium.

If an employer folds, the PPF guarantees to protect 100% of income for members already in receipt of a pension and 90% for those not yet at retirement. There are upper caps and other restrictions so it cannot be seen as perfect insurance, but it is certainly better than nothing – just ask the members of Robert Maxwell’s former business empire.

According to the latest available accounts, the PPF is responsible for paying pensions to 235,000 individuals and has assets worth £6.1 billion more than the liabilities it has taken on – in other words it has a significant funding surplus. Whilst that is great news it is worth remembering that the total deficit of all schemes in the UK stood at £226.5 billion at the end of March 2017. Much like the Titanic, there aren’t enough lifeboats for everyone, but the expectation is that most schemes won’t need the PPF so there is no cause for alarm.

Think, think, then think again.

We really can’t stress enough the importance of seeking professional advice if you are considering transferring a DB pension and, fortunately, the law agrees. Even if you think you can make the decision alone, you are legally required to take professional advice before any DC scheme will accept a transfer of more than £30,000.

Bear in mind, too, that most schemes will only guarantee a transfer value for three months. If a transfer has not been completed within this time the value will be recalculated, usually at your own expense. It is therefore worth getting things lined up before requesting the quote, if you are thinking of switching.