The news that inflation in the UK hit 4.2% in October will come as bad news, especially to those on fixed incomes. Particularly when it comes with warnings that the rise in the cost of living could reach 5% next spring. After that, inflation’s trajectory is uncertain say economists, with much depending on whether inflationary expectations kick in.

Although the pain for those on fixed incomes is bad enough, the return of what many economists and commentators only a few short months ago regarded as yesterday’s problem looks likely to have other less obvious but arguably even more damaging effects.

While increases in headline rates of tax are unambiguous and attract easy headlines, the adjustment of tax-free allowances and starting rates for tax bands by the government, so as to raise taxes, somehow seems to slip under the mainstream radar.

But higher taxes are exactly what will be the result of the Chancellor Rishi Sunak’s decision in his March 2021 Budget to freeze a whole host of allowances as well as the starting rates for income rates bands at their current levels until 2025/26. With inflation taking hold and reaching levels not seen since December 2011, those decisions look set to raise taxes for millions of people. It is not for nothing that money raised in this way is known as stealth tax.

A real world view

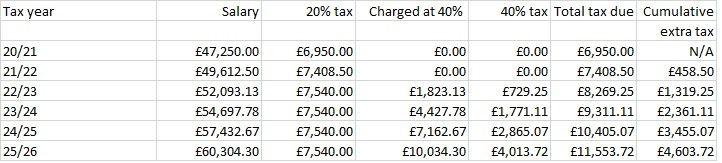

Let’s take an example to show how in an inflationary world, the freezing of the starting points for income tax bands could lead to significantly higher tax bills. And remember, this example doesn’t take into account the additional impact of the 1.5% percentage point rise in National Insurance on disposable incomes that is coming into effect in April.

By the end of the 2025/26 tax year, a person on an annual salary of £47,250 in 2020/21 will see their income tax bill increase from £6,950 20/21 to £11,553, a whopping 66% increase. This is assuming their salary increases by 5% each year. Overall, at the time of the recent autumn budget, the Office for Budget Responsibility (OBR) predicted that receipts from income tax would be a massive £99.8bn higher than its March 2021 prediction.

The reason is simple. As the table below illustrates, with the 40% starting rate frozen at £50,271 until April 2026, every year more and more of their rising income is subject to the 40% higher rate.

Assumptions: salary rising at 5% a year, excludes effects of National Insurance rate increase

Source: Courtiers

Frozen allowances

The freezing of tax allowances and reliefs could also prove potentially damaging to a person’s finances and those of their family. As an example, let’s take the lifetime allowance for pension contributions, which has been frozen at £1,073,100 until April 2026,

As a result, someone with a pension pot of £850,000 today, which grows at 5% a year, will breach their lifetime limit in less than five years’ time. This could lead to an unwanted tax bill, although that said, this can be mitigated with the relevant planning, analysis and pension protection.

Please contact your Courtiers Adviser, if you think you may be in danger of breaching the lifetime limit.

Capital Gains Tax (CGT) is another area where surging prices, ranging from property to stocks and shares and family heirlooms when combined with the freezing of allowances looks set to burn a nasty hole in people’s pockets. The OBR estimates CGT tax take will be £13.8bn higher than its March 2021 prediction.

Similarly, it estimates that the tax take from Inheritance Tax, another where frozen allowances are set to run up against estates that are booming in value, will be £2.7bn higher than it predicted in March 2021.

Human behaviour

In part, the impact of the Chancellor’s March 2021 decision will depend on how those affected or likely to be affected by higher taxes respond. Will someone who finds more of their income swallowed up by the 40% income tax rate cut back on their working hours, or will they look for a job with a higher salary to nullify the reduction in their take home pay and living standards? While how people respond remains an open question, this is not to say that there aren’t other ways for individuals and families to mitigate the unwelcome effects.

What you can do

Although it merely scratches the surface, those who are concerned by the impact of this unhealthy combination of taxation by stealth and rising inflation on their financial situation may wish to consider the following;

Make use of the ability to transfer allowances to others, particularly to your spouse or civil partner, who may not be using their full allowances.

Put more of your money into ISAs, which are exempt from income tax and capital gains tax. (An interesting footnote is that the annual £20,000 tax free ISA allowance has itself been frozen until April 2023 at least, thereby diminishing its value.)

Utilise the £3,000 annual gifting allowance.

Take maximum advantage of tax reliefs available to you. This allows you to deduct some payments you make from your gross income, so there is less for you to be taxed on. Examples are tax relief on pension contributions, on gift aid and on donations to charity

Conclusion

When facing the prospect of higher taxes getting ahead of the curve is vital, which makes tax planning more important than ever. Tax planning can be complicated, however, and the appropriate course of action will always depend on individual circumstances. You may find it helpful to discuss the issues raised in this article with your Courtiers Adviser.

Allowances and tax bands frozen until 5 April 2026 (unless stated otherwise).

Personal allowance £12,570

20% Basic rate limit £37,700

40% Higher rate limit £150,000

45% Additional rate on income over £150,000

Pension lifetime allowance £1,073,100

Capital gains tax exempt amount £12,300

Inheritance tax nil rate band £325,000

Dividend allowance £2,000 (until April 2023 at least)

Annual ISA allowance £20,000 (until April 2023 at least)