Beginning this week, many Courtiers clients will receive their Courtiers Tax Report for the 2022-2023 tax year. The Tax Report provides clients with important information about income and dividends they received from their investments on the Courtiers platform between 6 April 2022 and 5 April 2023. It also itemises investments sold and calculates realised capital gains or losses.

Following the end of the 2022-23 tax year on 5 April, many clients will already have received letters from HMRC notifying them that they can now file last year’s Self Assessment tax return. The Courtiers Tax Report provides key information to help them or often their accountant to complete this return.

Pretty essential

I asked Paul Kemsley, Senior Private Client Manager, how useful the Tax Report is for clients. “For those who need to complete an annual tax return, which is most of our clients, I would say they’re pretty essential,” he said. Importantly, Paul pointed out that not all Courtiers clients receive a Tax Report, only those who hold investments in a Courtiers Collective Portfolio. Because neither income or capital growth within individual savings accounts (ISAs) and self-invested pension plans (SIPPs) is taxable, clients with an ISA or SIPP will not receive a Tax Report in respect of those investments, and there is no need for any details to be disclosed to HMRC via a Self Assessment tax return, Paul explained.

In addition to covering the Courtiers funds, the Tax Report also includes details of income and dividends from directly held shares and non-Courtiers funds, bonds, exchange traded funds (ETFs), real estate investment trusts (REITs) and investment trusts held within a Courtiers Collective Portfolio.

Making it easier

The report’s designed in a way that makes it easier for clients to complete their tax return. For example, in the section headed UK Securities, alongside the figure for Untaxed Interest (£0.25 in the example above) is a reference to TR3 Box 2. This refers to Box 2 on Page TR3 of form SA100. If you have received other types of untaxed interest – say from a bank account, when filling in your tax return you will need to add that figure to the one that appears in your Courtiers Tax Report.

Form SA100 is the main Self Assessment tax return form. The full list of supplementary forms pages is available on the gov.uk website.

Some other examples of tax return boxes and forms

- Gilt Interest: Form SA101, Additional Information, Box 1

- Authorised Unit Trusts Dividends: Form SA100, Page TR3 Box 5

- Overseas Securities, Amount Before Tax: Form SA106, F2B

- Capital Gains, Form SA108, CG2 26

In more detail

Consolidated Tax Certificate – UK Securities

This section summarises income and any dividends paid to the client during the tax year broken down by type of income. For example, interest taxed at source and property income distributions. The figures shown are; Amount After Tax, Tax Taken Off and Gross Amount.

The sub-section headed Dividends Received summarises UK dividends, broken down into UK Company Dividends and UK Unit Trusts.

Consolidated Tax Certificate – Overseas Securities

During the tax year some clients may have received interest and dividend income from overseas investments and savings, for example, a fund domiciled abroad held on the Courtiers platform. This section provides a summary of interest and dividends from foreign holdings.

Realised Capital Gains Tax Calculations

This section lists all sales of investments funds and shares held directly during the tax year, and for each transaction calculates the capital gain or loss, taking into account Allowable Costs i.e. the cost of purchase. Again, there are references to the appropriate box – in this case on form SA108.

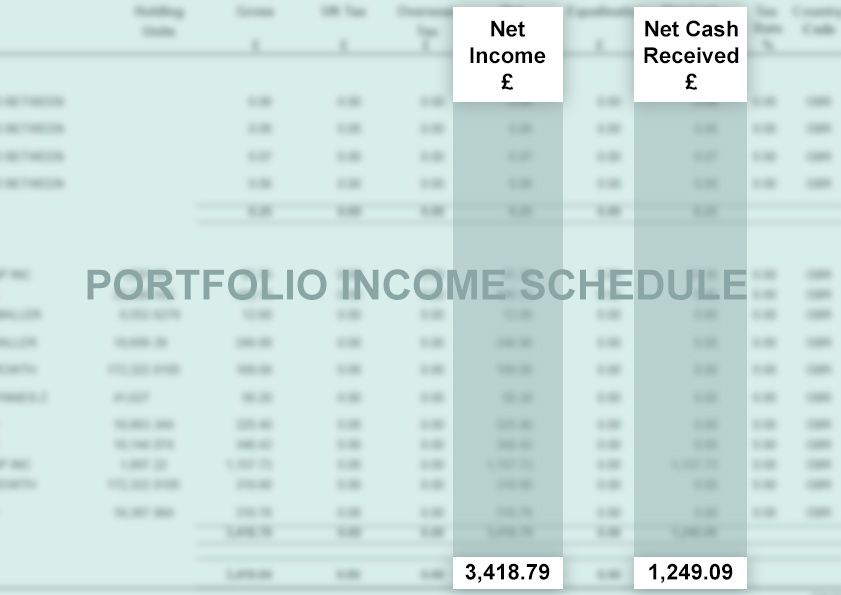

Portfolio Income Schedule

This section breaks down the summary information contained in the Consolidated Tax Certificate listing individual payments in date order. Each gross figure is then broken down further showing what tax (if any) was paid, the resultant Net Income and Net Cash Received.

Income from Accumulation funds

Dividend income from accumulation funds is not paid out as income into investors’ accounts – it is automatically reinvested in the fund as a ‘notional distribution’, increasing the value of existing accumulation units over time. With the exception of investors in the I Income Share Class of the UK Equity Income Fund, who receive cash payments, all Courtiers funds are accumulation funds.

A member of the Courtiers Investment & Fund Accounting Team explained how to calculate these notional distributions. Under UK Income – Dividends on the final page of the Tax Report, take the total Net Income figure for UK Income – Dividends (£3,418.79 in example below) and subtract from it the figure for total Net Cash Received (£1,249.09). The notional distribution for each individual dividend payment listed can be calculated in the same way.

The deadline for submitting Self Assessment tax returns for the 2022-23 tax year is midnight on 31 October 2023 if you’re making a paper return and midnight on 31 January 2024 if filing your return online.

If you have any questions about your Courtiers Tax Report or need any help or advice on completing your 2022/23 tax return, please contact your Courtiers Adviser.