In a recent article, we explained what cashflow modelling is and how it can be an important tool when discussing financial planning with clients. Let us now bring this to life with an example of a client’s situation and some of the points we might raise during a financial review meeting.

Preparation

Ahead of the meeting, we request an up-to-date snapshot from our client of their financial situation, including:

- Confirmation of yearly income

- Current expenditure, broken down to essential and non-essential

- Anticipated expenditure in retirement

- Planned future expenditure

- A revised breakdown of assets and liabilities (if applicable)

This preparatory work allows us to prepare an accurate cashflow model in advance and gives us more time to talk when we meet.

Setting the scene

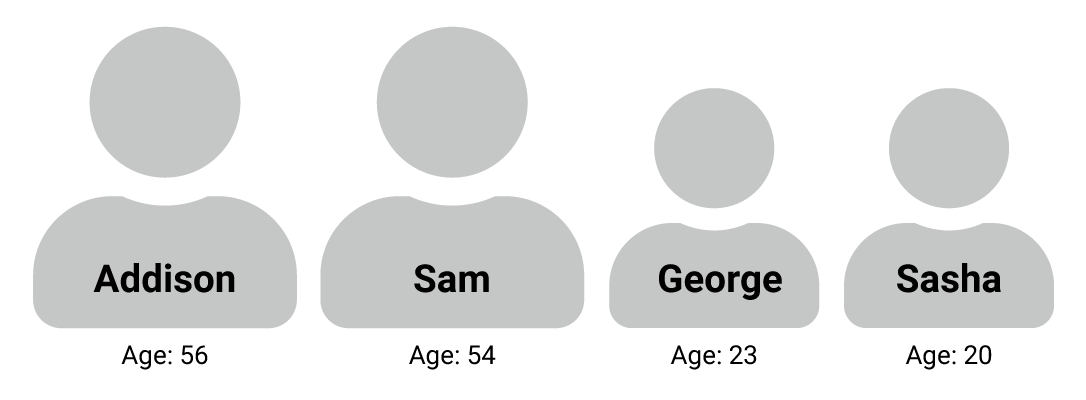

Our client is a married couple, Addison and Sam. They’re a family of four with two children, George and Sasha.

- Addison and Sam are currently employed

- Addison is a Director earning £80,000 per annum, with a non-guaranteed bonus of £40,000

- Sam is a Teacher earning £30,000 per annum

Expenditure

- Current core expenditure of £45,000 per annum

- Non-essential expenditure of £24,000 per annum

Proposed expenditure at retirement

- Non-essential expenditure is assumed to increase by £24,000 to £48,000 per annum, amounting to total expenditure of £93,000 per annum

Assets and liabilities

Assets

| Owner | Description | Value |

|---|---|---|

| Joint | Main residence | £645,000 |

| Joint | Bank account | £40,000 |

| Addison | Cash ISA | £30,000 |

| Sam | Cash ISA | £45,000 |

| Joint | Collective portfolio | £320,000 |

| Addison | SIPP | £450,000 |

| Sam | Teachers’ pension | £15,000 p/a escalating in line with inflation at 3% |

Liabilities

| Owner | Description | Value |

|---|---|---|

| Joint | Mortgage | £161,000 |

Client’s main objectives

- To retire when Addison reaches age 65, with an income to match expenditure of £93,000 per annum

- Expenditure from age 80 to revert to £69,000 per annum

- A consideration is to help the children out with the purchases of their first homes

Using cashflow modelling to explore what’s possible…

(Please note where the cashflow modelling refers to age, this is based on Addison’s age)

First we should evaluate the client’s net worth (total wealth, taking into account assets and liabilities):

The visual shows the overall net worth position at different ages. Red represents liabilities, which in this case represents the client’s mortgage at the beginning of the chart. Current liquid assets are made up of pensions, investments and bank accounts.

To age 80 – the client’s salary, income and other assets make up their net worth.

From age 80 onwards – their only asset is their property.

Discussion point: how do Addison and Sam feel about their liabilities increasing from age 79?

Income

Let us take a closer look at Addison and Sam’s position by considering the breakdown of their income:

Please note the income strategy represents one of the options that can be used to draw an income. The adviser is likely to assess all income strategies in line with a client’s objectives. The main point is to illustrate how long liquid assets can be used to provide an income before they run out.

Before 65 – the green bar chart shows us the client’s earned income up until retirement.

After 65 – both Addison and Sam have assets they can draw in a tax-efficient way in the form of ISAs (Light Blue) and Pension Commencement Lump Sums (25% tax free from their pensions) (magenta).

From 65 to 79 – they also can draw an income from their collective portfolio (dark blue).

From 67 – Addison starts to receive his State Pension and Sam receives her Teachers’ Pension.

From 69 – Sam gets her State Pension

From 79 – Addison and Sam are relying solely on their State Pensions and Sam’s Teachers’ Pension.

Discussion point: when Addison reaches 77 his pension fund would have been exhausted. This does not meet their objective of retiring at age 65.

Expenditure

National Insurance (NI) and Income Tax (Red) is higher whilst Addison and Sam are working. This reduces slightly when they start receiving an income from their pensions and investments.

Age 62 – their mortgage reaches the end of its term and is repaid.

Age 65 – their non-essential expenditure increases by £24,000 a year to age 79.

Discussion point: do they not foresee any large expenditure within the short term?

Cashflow – ‘the big reveal’

By building up a picture using the net worth, income and expenditure visuals, we help Addison and Sam begin to understand that their goals might not be possible.

The final visual, or the big reveal as we like to call it, presents cashflow in its simplest form. Addison and Sam can quickly see that they will run out of money by age 78.

The next step will be to consider each discussion point above and any planning options available, to help guide Addison and Sam towards meeting their goals in retirement. We’ll focus on these in the next article.

For any answers or further information in the meantime, please speak to your adviser or contact us.