David Cameron’s resignation as UK Prime Minister on 24th June 2016 heralded-in a tempestuous period for British politics. A decade later, it’s still not over as almost 10 years to the day Keir Starmer announced his resignation and we will shortly appoint our 6th post-Brexit PM. To put that in context, the last six pre-Brexit Prime Ministers spanned 40 years.

In April 2016 I issued a research note entitled “Britain and the European Union – In or Out? The Facts & Fiction” and an article entitled ‘Brexit’. In the research note I looked at how the UK economy had performed inside the EU and whether there were grounds, as the Brexiteers contested, for leaving the union. I concluded that Britain had done rather well inside the EU, and although there were solid grounds for supposing it could do even better on its own, that required the free movement of goods, services and people that the average Brexiteer was unlikely to contemplate. In any event, I reckoned that a clean break from Europe required a government voted in at a general election on a Brexit ticket, and that a vote for leave at a referendum arranged by a pro-EU Tory government would be messy. On this point, at least, I was right. So how has our economic performance stacked up against our ex-EU partners post Brexit? The answer is not great, but not disastrous either.

To understand the performance of the British economy you need to consider our competitiveness through three distinct periods:

- The “Great Moderation” from 1990 to 2008 during which inflation was benign, interest rates began dropping and the economy advanced with consistently low variability – in other words, it was a period of generally steady growth.

- The “Post-Global Financial Crisis Blues” from 2008 to 2016.

- The “Post-Brexit era” from 2016 to 2025.

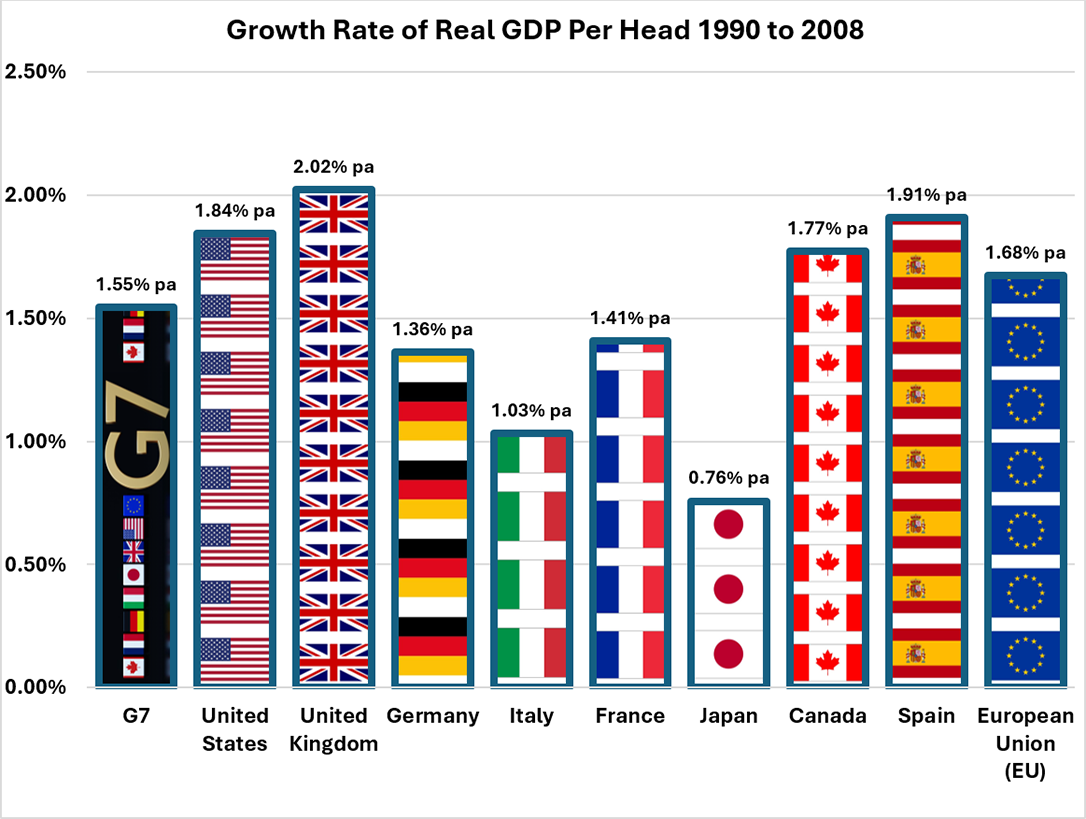

The Great Moderation

From 1990 to 2008 our economic performance outstripped most of our competitors. Britain became a popular place to invest as it offered relative political security, stable government, access to the EU (then the world’s largest single market) and a wide range of competitive, readily available, financial & business services. GDP per-capita[1] grew by over 2% p.a. in this period, better than any other major developed economy.

Chart 1 – 1990 to 2008 – The “Great Moderation”

Source: IMF/Courtiers

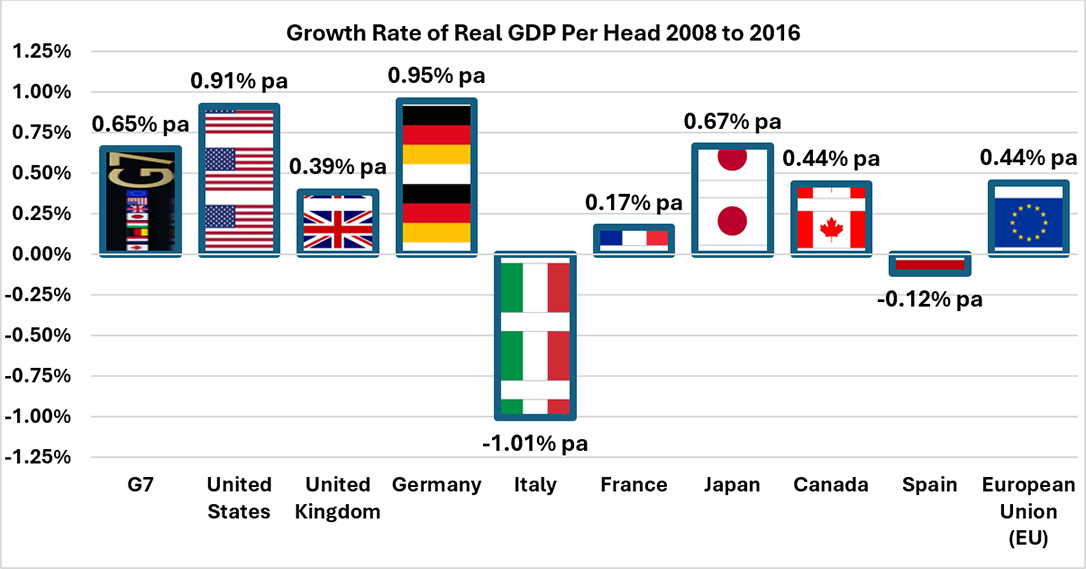

Post GFC Blues

As an economy with large exposure to banking, insurance, housing and capital markets, Britain suffered worse than most during, and after, the 2008 Global Financial Crisis. In the period 2008 to 2015, output per head in the UK grew by just 0.39% p.a., lower than the EU average of 0.44% p.a. but better than France & Italy (0.17% p.a. & -1.01% p.a. respectively).

Germany, with its highly developed manufacturing base and underdeveloped financial sector, outstripped other economies, but the USA was only just behind, despite being the epicentre of the 2008 collapse in financial markets. America has a quite remarkable ability to bounce-back, and fast!

Chart 2 – 2008 to 2016 – The Post Global Financial Crisis Blues

Source: IMF/Courtiers

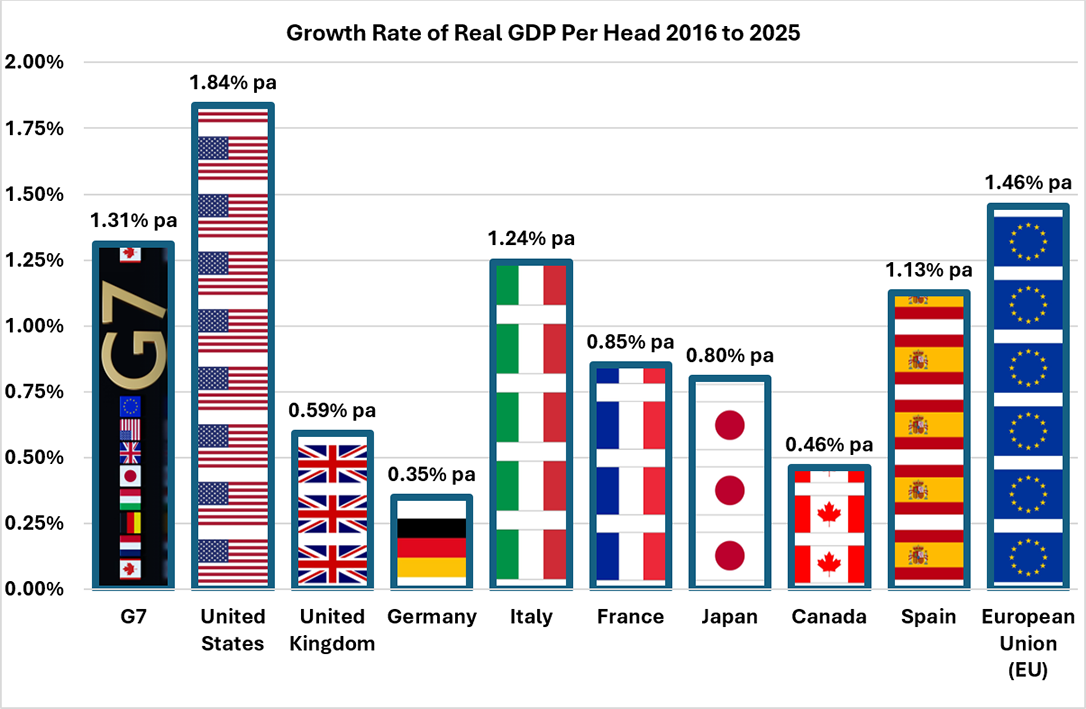

Post-Brexit Era

The post-Brexit political turmoil took its toll on the UK, which has not flourished outside of the EU compared to most of our ex-partners. Remainers blame Leavers for the UK’s post Brexit woes, and Leavers blame Remainers. Both are guilty of oversimplification of our problems, and this creates a merry-go-round of accusation and counter accusation, which is unhelpful.

Although our post-2016 economic performance has lagged most of our major competitors, we have fared better than the mighty German powerhouse and we are ahead of Canada. If Brexit had been the disaster for Britain that many claimed it would be, one would have expected us to be bottom of the G7 league (Canada, France, Germany, Italy, Japan, the United Kingdom and the United States) rather than 3rd from bottom.

Chart 3 – 2016 to 2025 – The Post Brexit Era

Source: IMF/Courtiers

Conclusion

Even though the mayhem that followed the June 2016 referendum would have been a headwind for the economy, the reasons for the UK’s poor post-Brexit performance are many: we have failed to efficiently deliver large infrastructure projects (HS2, London’s new runway & Hinkley Point C to name but three), our high energy costs make the UK an expensive place to make things, draconian planning restrictions are blocking the building of new homes, business investment has generally been weak, productivity improvements have stalled and real wage increases have been frugal. Hardened Remainers will say that Brexit has contributed to all these woes, but you can’t blame leaving Europe for everything, especially as it’s now clear that other countries that were not leaving an economic & political union, like Canada and Germany, have fared worse than us over the last 10 years.

Nonetheless, it’s likely that Brexit did have a short-term negative effect on output and trade, but it could still work to Britain’s advantage in the long run, especially if the country adopts the policies advocated by Professor Patrick Minford, the poster-child Brexiteer economist who advocated getting out of the EU to allow tariff free trade and free movement of people, policies that would, ironically, be anathema to many die-hard leavers.

In short, Brexit presented problems and opportunities, but we are the ultimate architects of our own future. If we can get our businesses investing more, use the latest technologies to improve services, shrink government and deepen the available capital base available to our start-ups, we will thrive, irrespective of whether we are inside or outside of the European Union.

[1] I use GDP per-capita from the IMF WEO series based on constant prices in International Dollars @ PPP (purchasing power parity). This series adjusts for inflation (so it shows “real” growth) and by focusing on output per capita (i.e. per head) we see the real improvement in wealth for a country’s population, which can be distorted using just GDP because, for example, a huge influx of immigrant workers may boost overall GDP whilst driving down GDP per head, especially if the new workers are employed in low-output jobs.